RSS Feed

RSS Feed

October 9th, 2021

October 9th, 2021  Awake Goy

Awake Goy 06.10.2021

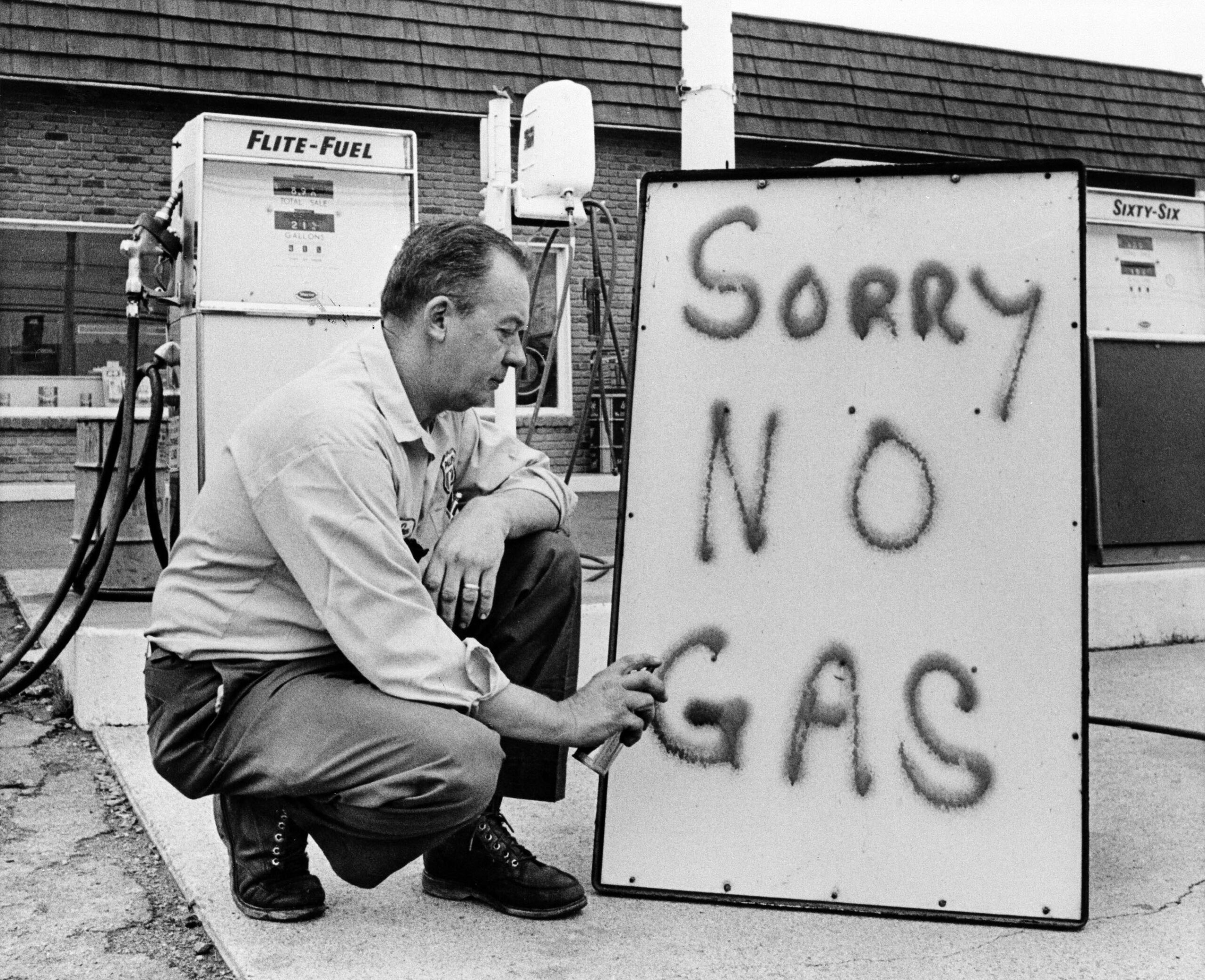

The current situation in the energy market is quite worrisome. Europe is taking the brunt of it, and is concerned that a long and cold winter could send it off the edge into an economic crisis, as natural gas prices are soaring to never-before-seen heights.

The Asian market, which is the largest in the world is also in a tattered state, with China already feeling the consequences of reducing dependency on coal and lack of energy resources.

This all is a result of several factors that have led to the present reality of events and the exacerbating situation.

The spot price for natural gas continues breaking records, by reaching $1,600 per 1,000 cubic meters before dropping back to $1,400 on October 6th.

Spot is initially a high-risk market; it is based on the sellers of the product that create an artificial surplus or lack of said product. If the product was deficient by definition, for example there’s not enough of it to begin with, then buyers could potentially control the market, but this is a different story.

Furthermore, gas prices are much less controlled compared to oil prices, which fluctuated rapidly in 2020. Various energy resources’ prices depend on their own specifics, but it is an obvious fact that these prices connected.

The market is concerned about energy supply this winter and shrugged off October 4th’s news from Nord Stream 2 AG, the operator of the controversial Russia-led gas pipeline, which started filling the first string of the pipeline with gas to get ready for the moment that German authorities grant it an operational license.

While gas prices are soaring, US oil prices rose for the fifth day in a row to levels not seen since 2014, amid global concerns about energy supply due to signs of tension in the oil, natural gas and coal markets.

Brent prices also rose due to concerns about supplies, especially after OPEC+ decided to stick to the planned increase in production. To put it simply, there might be an artificial deficiency which causes an increase in price.

Following a short meeting on October 4th, the OPEC+ ministers approved an increase in production by 400 thousand barrels per day in November, after which the price of oil on the New York Stock Exchange reached its highest in almost seven years. On the eve of the talks, speculation spread that the cartel and its allies could increase production by 800 thousand barrels per day in November, but, according to delegates, such a proposal was not announced.

According to Amrita Sen, a leading oil analyst and co-founder of Energy Aspects, Saudi Arabia seeks to make as few changes as possible to the current OPEC+ agreement on monthly production increases.

Instead of pushing for increased production and lowered prices, the United States appeared satisfied with Riyadh’s plan and hasn’t exerted any political pressure to change the situation.

The American Petroleum Institute reported that oil reserves in the United States increased by 951 thousand barrels in the week of October 1st.

Despite increasing prices, the United States is increasing its reserves in the face of the potential increase in prices even further.

The biggest “victim” is the European consumer.

Europe is already feeling the pressure, as natural gas is incredibly important to industry, increasing oil prices complicate the situation even further.

Not only does industry need to use a lot of natural gas, but some part of it also needs to be distributed to households, and the colder the weather gets, the more gas is required. Civilian infrastructure, as well as households needing increasing amounts of natural gas led to a higher deficiency in industry, which could itself lead to an increase in the price of various products, as well as many businesses straight up closing.

Northern Europe is already feeling the strain, as the depletion of reservoirs hinders the production of hydroelectric power.

The water level in Norwegian hydroelectric power plants for this time of year is at a minimum level. This is a concern just a few weeks before the reduction of reservoirs in late autumn. There is not enough water for export to the continent and to the UK.

Ireland and the UK are the hardest hit by the global gas shortage and are experiencing a shortage of electricity.

In Asia, which is the trade center of LNG, the situation is also quite difficult.

LNG-AS spot prices reached a record high, approximately 100% higher than one month ago, and 500% higher year over year.

A standard LNG cargo of 3.4 trillion BTU (British Thermal Units) now costs $100-120 million, while at the end of February its cost was less than $20 million.

It is not clear if any buyer is capable of actually paying for the LNG they’ve bought, as such sellers are requesting letters of credit, guaranteeing that there will be solvency when the time to pay comes.

India following China is on the verge of an energy crisis as coal reserves have reached a critical level.

According to the Ministry of Energy of India, 135 thermal power plants in the country on average had coal reserves for only four days. The shortage of electricity has already begun to affect the economy of neighboring China, where last month the manufacturing sector experienced the first decline in indicators since the beginning of the pandemic.

What could be the reason for all of this?

Notably, the renewable energy agenda, launched in the early 2000s in conjunction with the shale production program in the United States.

Both of these were ways in which the West reduced its energy dependence on exports.

It was necessary to minimize the impact of the inevitable price spike by the time the global gas market was created.

Each acceleration of new mining projects was accompanied by an increase in prices, which provided an investment flow into more expensive production.

However, the renewable energy program structurally failed. To put it simply: the United States’ ambition fell apart, as the largest gas resources are located in Russia and Iran, and both are countries that Washington has little, if any, influence over. Qatar and Australia are not enough to turn the tide.

In this strategy of reducing energy dependence at the time of the formation of the global gas market, Europe relied on renewable energy, and the United States – on shale.

The share of renewable energy in the total energy balance of the USA does not exceed 8%, in Europe it is approximately 20%, and globally it sits around 5%, in the area of statistical mistake.

In accordance with the shares of renewable energy, we are seeing a gas price boom today. The United States, with the help of shale, forced not only OPEC and Russia, but also Europe and Japan to pay for the new market structure. It’s just like in 1973, when the spot-exchange oil market was created.

The current natural gas market is in shambles, as it suffered a terrible combination of circumstances.

Fuel reserves in Europe were reduced in the face of the very real possibility of a prolonged winter, a decrease in supplies from Russia and an increase in demand for LNG in Asia, which prevented the restoration of reserves in the summer.

This was joined by a decline in production in the North Sea, due to a maintenance that was delayed because of the pandemic.

This is all exacerbated by the hasty transition towards renewable energy sources without the necessary technology to adequately do so.

A surprising factor is also the fact that prices were also affected by a decrease in the average wind speed to the lowest since the 1960s, interruptions in the operation of nuclear power plants and a fire on an underwater power cable connecting the UK and France.

To put it in simple terms, the “Green Deal” is motivated not by a scientific or economic approach, but by populism aimed at voters: pseudo-leftists and neo-liberals.

This is in addition to the hesitancy of multi-national corporations to invest in infrastructure, fixed assets and production. It is much more preferable to fix the profit margin and distribute funds among shareholders and management.

Finally, Hurricane Ida was a sort of jump-start of the energy crisis, as it led to the shutdown of production of massive amounts of energy in the Gulf of Mexico.

According to the U.S. Bureau of Safety and Environmental Protection, as of September 12th, 48.6% of oil production and 54.4% of gas production in the Gulf of Mexico were still stopped.

Due to the hurricane, more than 40 million barrels of refined fuel were lost and slightly fewer were lost in blocked production.

Exporters were forced to redistribute trade flows around the Atlantic and America to ensure supplies.

All of these factors combined are promising a very cold winter, and a very bleak, and extremely expensive future, compared to which the 2008 financial crisis may seem like a minor inconvenience.

As a consequence, industry will suffer, but the final consumer will suffer the most.

The rise in gas and electricity prices in Europe sends a powerful signal to manufacturers to consider temporarily closing factories, and to owners of homes and offices to turn off thermostats to prevent stocks from falling to a critical minimum and depletion of fuel reserves this winter.

For manufacturers, a short-term closure has a double benefit: a reduction in electricity costs, as well as an increase in prices for their products, which helps protect profits from rising electricity and gas prices. Still, a balance needs to be found as a business cannot remain closed indefinitely.

After a sufficient number of reliable plant closures and other energy-saving measures are announced, futures prices are likely to decline, as there will not be enough buyers, regardless of the price.

The supply chain will be disrupted if factories close, and this brings along its own set of problems.

If the upcoming winter does not turn out to be mild, rising prices and physical shortages of gas, coal and electricity are unlikely to remain limited to energy markets, and this will affect the rest of the economy, as is already happening in China.

Separately, this is a wake-up call that climate change is rapidly turning into a direct factor influencing asset allocation decisions for investors. It used to be a fringe possibility, somewhere in the background.

Investors can no longer afford to ignore the disasters befalling the world, because all of these result in rising prices for natural gas and other commodities.

The centralized EU policy to achieve zero emissions by 2050, significantly aggravated and accelerated the development of the crisis. It promises to become even worse as Germany promises to close down nuclear power plants by the end of 2021. Berling stop supplying electricity to the very European networks that have taken the brunt of the crisis. The resulting gap will be felt by the whole of Europe.

MORE ON THE TOPIC:

Filed under: China, EU, India, Norway, UK | Tagged: American shale oil, Gas Market, KSA, Nord Stream, Nord Stream 2, Opec+ |

Posted in

Posted in  Tags:

Tags: